Integrated Annual Report 2021

For the second year now, the Italgas Group (hereinafter also referred to as “Italgas” or the “Group”) has presented the annual financial report in the form of an Integrated Annual Report (hereinafter also referred to as the “Report” or the “Integrated Report”) as a tool for the integrated reporting of financial and non-financial data. The Integrated Annual Report includes information which was previously, before 2020, included in the following documents:

More specifically, the Integrated Annual Report consists of the

Integrated Directors’ Report, with both financial and non-financial

reporting, the Consolidated Financial Statements and the

Separate Financial Statements of Italgas S.p.A..

By way of this document, the Italgas Group also aims to meet the requirements of Italian Legislative Decree 254/16, issued in order to “implement Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups”. Also, “to the extent necessary to ensure understanding of the business, its performance, results and the impact it produces, the document covers environmental and social matters, personnel-related issues, respect for human rights and the fight against active and passive bribery, which are important, considering the activities and characteristics of the company”.

The Integrated Annual Report makes it possible to provide stakeholders with an accurate, extensive and transparent report of the Group’s activities, the results achieved and their progress, in addition to the services provided.

Having joined the United Nations Global Compact, Italgas also decided to update the annual Communication on Progress (CoP)9 within its Integrated Report, by supplementing its content in order to notify all internal and external stakeholders of the activities undertaken and results achieved when implementing the Ten Principles of the Global Compact.

In relation to the financial information, the Italgas Integrated Annual Report was prepared using the following references:

Pursuant to Italian Legislative Decree 254/2016, the reporting of non-financial information is carried out “in accordance with the methods and principles required by the reporting standard used as a reference or by the independent reporting method used to prepare the statement”.

For this aspect, the Group used the following technical and methodological references:

For the information on the topics required by Italian Legislative

Decree no. 254/2016, a specific reconciliation table has been

prepared.

Where estimations were required in order to report particular data, this is specified in the description or in the notes to the table.

In addition, with reference to the requests for information correlated with European Taxonomy, the report is made in compliance with the provisions of the “Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088” as well as with the Delegated Acts applicable to it with reference to the date of publication of this document.

The document is published annually and is available on the website https://www.italgas.it/it/investitori/bilanci-e-presentazioni/.

To facilitate the reading of this document, specific icons have been used to identify the minimum elements required by Italian Legislative Decree 254/16 ![]() and the principles required by the Global Compact

and the principles required by the Global Compact

Finally, the Group also provides a summary of its governance, strategy, risks and opportunities, metrics and targets relative to climate change, in response to the recommendations made by the Task Force on Climate-related Financial Disclosures: this information is provided in summary form in the table “Information on the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD)”, at the foot of this document.

The data and information reported in this Integrated Annual Report refer to the performance of the Italgas Group in the financial year ending 31 December 2021.

Compared with last year, the consolidation scope has changed as a result i) of the incorporation of Toscana Energia Green into Seaside, ii) of the establishment of Bludigit, iii) of the acquisition of all the capital of the company Isgastrentatré followed by its incorporation into Medea and iv) of the acquisition of Ceresa.

For the non-financial reporting, the quantitative data in this document refer, where possible, to the 2019, 2020 and 2021 financial years. This is to ensure comparison of the information with information from previous financial years, as required by Italian Legislative Decree 254/16, and also to comply with the comparability principle under the GRI Standards.

The reporting boundary of the non-financial data includes:

Data relating to the Energy Service Company (ESCo) Ceresa S.p.A., with registered office in Turin, at Corso Palestro 10, is not included in the 2021 non-financial reporting boundary insofar as the completion of acquisition of control took place in December 2021 and has no significantly material effects on the report.

Any exceptions to the criteria set out above are detailed in the individual sections of the document in the form of a footnote to a table or page.

Preparation of the Italgas Integrated Annual Report involved across-the-board engagement of all Italgas Group companies, departments and divisions and the performance of the following activities:

More specifically, the following independent auditors’ reports contain the results of the audits conducted by Deloitte & Touche S.p.A:

Report in accordance with Article 3, paragraph 10 of Italian Legislative Decree no. 254 of 30 December 2016 and Article 5 of CONSOB Regulation no. 20267/2018, drawn up in relation to non-financial information reporting in the document;

Reports in accordance with Article 14 of Italian Legislative Decree no. 39 of 27 January 2010 and Article 10 of Regulation (EU) No 537/2014, drawn up in relation to the financial information in the Consolidated Financial Statements and Separate Financial Statements.

The structure and contents of the Integrated Annual Report must revolve around the analysis of the material issues, i.e. those considered relevant and a priority for the company, taking into account not only the minimum elements set out in Italian Legislative Decree 254/2016 (Article 3, paragraph 1), but also its own business and characteristics, as well as the expectations of its stakeholders.

As the Group looks to sustainability as an evolutionary concept, Italgas has chosen to update the materiality matrix once a year, in order to incorporate, for example, stakeholder requests, the evolution of the regulatory context, the group’s strategy and any drivers potentially able to significantly impact the Group’s capacity to create value in the short, medium and long-term.

In particular, Italgas updates its Materiality Matrix by means of a series of activities coordinated by the Sustainability Department. These activities include but are not limited to:

Following in-depth stakeholder engagement activities carried out for the 2020 non-financial report, for 2021, Italgas refined its materiality matrix through internal stakeholder engagement, involving the top management of the companies of the whole Group. This resulted in a reassessment of the relevance of certain topics and the inclusion of new aspects, with a view to guaranteeing an even greater level of alignment with the 2021-2027 Strategic Plan and with the evolution of the sustainability route undertaken.

This refinement led to some minor variations in the definition of the material topics, as well as to the following main changes:

The very same relevance of topics, consequently, has changed in adhesion to the contents of the 2021-2027 Strategic Plan.

Dialogue with stakeholders is an opportunity that is useful for understanding the level of satisfaction of a company’s work. It is also a chance to gather useful insights in order to improve the services and operational and management models. Accordingly, Italgas adopts diversified and flexible dialogue and involvement practices, in response to the various characteristics and needs of its stakeholders.

The stakeholder categories identified and stakeholder engagement activities carried out in 2021 are set out below.

| Stakeholder category | Stakeholder interaction methods |

|---|---|

| Investors and lenders | Periodic financial reports and conference calls about these; presentation of the business plan; shareholders’ meeting; physical and on-line meetings and conference calls with analysts and investors, also focusing specifically on SRI matters; corporate website; social networks. |

| Suppliers | Dedicated meetings, supplier conventions; annual engagement initiatives. |

| Customers and sales companies | Direct, ongoing relationship with the sales personnel through dedicated dialogue channels (e.g. “GasOnLine”); periodic workshops with sales companies; interactions with end customers through the customer portals (MyItalgas, MyToscanaEnergia, MyMedea, etc.); customer satisfaction surveys. |

| Authorities and Associations | Incontri periodici; dialogo continuo e workshop di dibattito e confronto in merito a tematiche di sostenibilità a livello italiano e internazionale. |

| People | Training events; periodic meetings; annual meetings to discuss career development paths; newsletters; company environment analyses; company Intranet. |

| Communities and local areas | Meetings with representatives of local communities, associations and organisations; social and cultural initiatives. |

Another method of interaction compared with those summarised, which is valid for all stakeholders, is the answering of questionnaires aiming to assess sustainability performance and the publication of the results obtained in them.

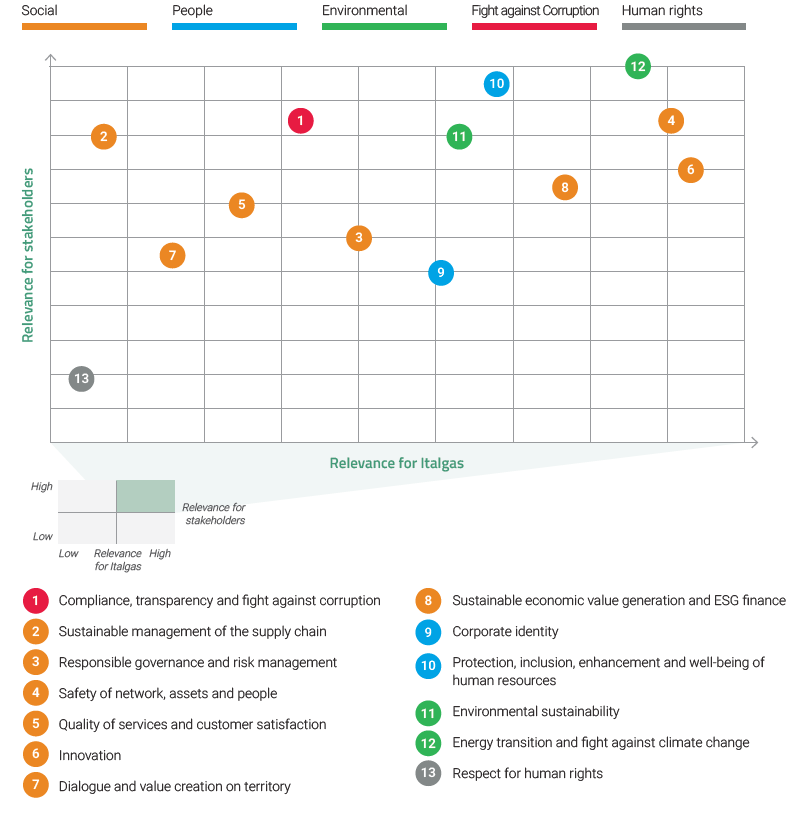

Italgas has therefore updated its materiality matrix, highlighting the degree of relevance assigned to priority topics, from an internal perspective (x-axis) and an external perspective, i.e. of the reference stakeholders (y-axis).

The highest relevance, from an internal and external perspective, was given to the following five topics:

The topic of “Respect for human rights”, which is in any case constantly monitored and supervised by the Group, has been, however, assessed with low relevance.

The aspect relating to water resources contained in the “Environmental sustainability” topic is also, on its own, considered as not relevant to the core business of Italgas, as more fully explained in the section on “Attention to the environment” of this document. Considering, in fact, the entity of the volumes of water withdrawn, the type of use made and the geographic location of the Italgas companies, the impacts on the water resource were considered negligible. Although the water resources management topic may be of greater relevance to Italgas Acqua, this topic was not included in the non-financial reporting in the Integrated Annual Report, given the impact of this business on the Group’s total revenue (less than 1%). Despite this, as evidence of the fact that the aspect is in any case monitored and supervised, the above section sets out the withdrawals, discharges and consumptions of the Group, in compliance with the requirements of Italian Legislative Decree no. 254/16.

With regard to the areas provided for by the Decree, Italgas’s material topics are broken down as follows:

The material topics “Responsible governance and risk management” and “Corporate identity” are transversal with respect to the areas envisaged by the Decree.

Below is the table of GRI indicators reported.

| GRI content index | |||

| GRI ID | Description of indicator | Notes | Page |

| General standard disclosures | |||

| Profile of the organisation | |||

| 102-1 | Name of organisation | 16 | |

| 102-2 | Activities, brands, products and services | 30-31 | |

| 102-3 | Location of headquarters | 16 | |

| 102-4 | Location of operations | 16 | |

| 102-5 | Ownership and legal form | 16 | |

| 102-6 | Markets served | 40-41 | |

| 102-7 | Scale of the organisation | 40; 74; 92 | |

| 102-8 | Information on employees and other workers | 111-112; 131 | |

| 102-9 | Supply chain | 144-157 | |

| 102-10 | Significant changes to the organisation and its supply chain | In 2021, no significant changes were made to the organisation and its supply chain. | |

| 102-11 | Principle of precaution | 62-74 | |

| 102-12 | External initiatives | 52-55 | |

| 102-13 | Membership of associations | 110 | |

| Strategy | |||

| 102-14 | Statement from senior decision-maker | 9-11 | |

| Etica e integrità | |||

| 102-16 | Values, principles, standards and norms of behaviour | Values, mission and purpose; 77 | |

| Governance | |||

| 102-18 | Governance structure | 56-62 | |

| 102-22 | Composition of the highest governance body and its committees | 56-62 | |

| 102-24 | Nominating and selecting the highest governance body | 56-62 | |

| Stakeholder engagement | |||

| 102-40 | List of stakeholder groups | 19 | |

| 102-41 | Collective bargaining agreements | In the three years 2019-2021, the percentage of employees covered by collective bargaining agreements is 100%. | |

| 102-42 | Identifying and selecting stakeholders | 17-21 | |

| 102-43 | Approach to stakeholder engagement | 17-21 | |

| 102-44 | Key topics and concerns raised | 17-21 | |

| Reporting practices | |||

| 102-45 | Entities included in the consolidated financial statements | 4; 16 | |

| 102-46 | Defining report content and topic boundaries | 17-21 | |

| 102-47 | List of material topics | 17-21 | |

| 102-48 | Restatements of information | 17 | |

| 102-49 | Changes in reporting | No significant changes occurred in 2021. | |

| 102-50 | Reporting period | 16 | |

| 102-51 | Date of most recent report | The 2020 Integrated Annual Report was published in April 2021. | |

| 102-52 | Reporting cycle | 14 | |

| 102-53 | Contact points for questions regarding the report | sustainability@italgas.it | |

| 102-54 | Claims of reporting in accordance with the GRI Standards | 15 | |

| 102-55 | GRI content index | 21-26 | |

| 102-56 | External assurance | 17; 197 | |

| Economic performance | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 162 | |

| 103-2 | The management approach and its components | 21; 162 | |

| 103-3 | Valutazione delle modalità di gestione | 21; 162 | |

| 201-1 | Direct economic value generated and distributed | 162 | |

| Anti-corruption | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 81-83 | |

| 103-2 | The management approach and its components | 21; 81-83 | |

| 103-3 | Evaluation of the management approach | 21; 81-83 | |

| 205-2 | Disclosure and training on anti-corruption policies and procedures | 82 | |

| 205-3 | Confirmed incidents of corruption and actions taken | 81 | |

| 207-1 | Approach to taxation | 163-164 | |

| 207-2 | Tax governance, risk control and management | 163-164 | |

| 207-3 | Stakeholder engagement and management of tax concerns | 163-164 | |

| 207-4 | Country-by-country reporting | Not applicable, Italgas only operates in Italy. | |

| Energy | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 165-173 | |

| 103-2 | The management approach and its components | 21; 165-173 | |

| 103-3 | Evaluation of the management approach | 21; 165-173 | |

| 302-1 | Energy consumed within the organization | 183 | |

| 302-3 | Energy intensity | 183-184 | |

| 302-4 | Reduction of energy consumption | 178 | |

| Water withdrawals and discharges | |||

| 303-1 | Interactions with water as a shared resource | 21; 165-166; 181-182 | |

| 303-2 | Management of water discharge-related impacts | 21; 165-166; 181-182 | |

| 303-3 | Water withdrawals | 185 | |

| 303-4 | Water discharge | 185 | |

| 303-5 | Water consumption | 185 | |

| Emissions | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 165-166; 3174-179 | |

| 103-2 | The management approach and its components | 21; 165-166; 3174-179 | |

| 103-3 | Evaluation of the management approach | 21; 165-166; 3174-179 | |

| 305-1 | Direct (Scope 1) GHG emissions | The CO2e emissions were consolidated using the operational control approach. The GHGs included in the calculation are CO2 and CH4 and the emissions are calculated with a GWP of methane equal to 28, as indicated in the scientific study of the Intergovernmental Panel on Climate Change (IPCC) “Fifth Assessment Report IPCC”. Losses from venting can be considered residual, while there are no pneumatic or unburned material losses. | 177; 185 |

| 305-2 | Energy indirect (Scope 2) GHG emissions | 177; 185 | |

| 305-3 | Other indirect (Scope 3) GHG emissions | As regards the calculation of scope3 emissions linked to value spent, an internal approach was used that associates a conversion factor from the value spent into CO2e emissions for each product category. | 177; 185 |

| 305-4 | GHG emissions intensity | 185 | |

| 305-5 | Reduction in GHG emissions | 178 | |

| 305-7 | Nitrogen oxides (NOX), sulphur oxides (SOX), and other significant emissions | SOX and COV emissions are not considered significant | 186 |

| Waste | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 165-166; 180-181 | |

| 103-2 | La modalità di gestione e le sue componenti | 21; 165-166; 180-181 | |

| 103-3 | Valutazione delle modalità di gestione | 21; 165-166; 180-181 | |

| 306-4 | Rifiuti inviati a recupero | 186,187 | |

| 306-5 | Waste for disposal | 186,187 | |

| Compliance ambientale | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 165-166 | |

| 103-2 | The management approach and its components | 21; 165-166 | |

| 103-3 | Evaluation of the management approach | 21; 165-166 | |

| 307-1 | Non-compliance with environmental laws and regulations | In 2021, just like in 2020 and 2019, the Italgas Group did not receive any significant sanctions for breaching environmental laws and regulations. | |

| Valutazione ambientale dei fornitori | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 144 -157 | |

| 103-2 | The management approach and its components | 21; 144 -157 | |

| 103-3 | Evaluation of the management approach | 21; 144 -157 | |

| 308-1 | New suppliers that were screened using environmental criteria | 157 | |

| Employment | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 111 | |

| 103-1 | The management approach and its components | 21; 111 | |

| 103-3 | Evaluation of the management approach | 21; 111 | |

| 401-1 | New employee hires and employee turnover | 113; 115-116 | |

| 401-3 | Parental leave | 129 | |

| Health and safety in the workplace | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 134-135 | |

| 103-2 | The management approach and its components | 21; 134-135 | |

| 103-3 | Evaluation of the management approach | 21; 134-135 | |

| 403-1 | Occupational health and safety management system | 21; 134-135 | |

| 403-2 | Hazard identification, risk assessment, and incident investigation | 21; 134-135 | |

| 403-3 | Occupational health services | 21; 134-135 | |

| 403-4 | Worker participation, consultation, and communication on occupational health and safety | 21; 134-135 | |

| 403-5 | Worker training on occupational health and safety | 21; 134-135 | |

| 403-6 | Promotion of worker health | 21; 134-135 | |

| 403-7 | Prevention and mitigation of occupational health and safety linked by business relationships | 21; 134-135 | |

| 403-9 | Workplace accidents | 135-136 | |

| Education and training | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 111; 117-123 | |

| 103-2 | The management approach and its components | 21; 111; 117-123 | |

| 103-3 | Evaluation of the management approach | 21; 111; 117-123 | |

| 404-1 | Average hours of training per year per employee | 120 | |

| Diversity and equal opportunities | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 111; 130-134 | |

| 103-2 | La modalità di gestione e le sue componenti | 21; 111; 130-134 | |

| 103-3 | Valutazione delle modalità di gestione | 21; 111; 130-134 | |

| 405-1 | Diversità negli organi di governo e tra i dipendenti | 58; 131-134 | |

| 405-2 | Ratio of basic salary and remuneration of women to men | 133 | |

| Non discrimination | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 111-127 | |

| 103-2 | The management approach and its components | 21; 111-127 | |

| 103-3 | Evaluation of the management approach | 21; 111-127 | |

| 406-1 | Incidents of discrimination and corrective actions taken | 127 | |

| Child labour | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 144 – 157 | |

| 103-2 | The management approach and its components | 21; 144 – 157 | |

| 103-3 | Evaluation of the management approach | 21; 144 – 157 | |

| 408-1 | Operations and suppliers considered to have significant risk for incidents of child labour | To become part of the Italgas supply chain it is necessary to accept the principles of the Group’s Code of Ethics, as well as the Code of Ethics of the Italgas Suppliers and the Ethics and Integrity Agreement, in compliance with our Organisational Model 231. All suppliers are required to meet important criteria in terms of human rights and work by accepting the Italgas Policy on Human Rights, health and safety, environmental protection and the ethical and responsible management of the business. No supplier has been identified as having significant risk for incidents of child labour. | |

| Forced or compulsory labour | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 144 – 157 | |

| 103-2 | La modalità di gestione e le sue componenti | 21; 144 – 157 | |

| 103-3 | Evaluation of the management approach | 21; 144 – 157 | |

| 409-1 | Operations and suppliers considered to have significant risk for incidents of forced or compulsory labour | To become part of the Italgas supply chain it is necessary to accept the principles of the Group’s Code of Ethics, as well as the Code of Ethics of the Italgas Suppliers and the Ethics and Integrity Agreement, in compliance with our Organisational Model 231. All suppliers are required to meet important criteria in terms of human rights and work by accepting the Italgas Policy on Human Rights, health and safety, environmental protection and the ethical and responsible management of the business. No supplier has been identified as having significant risk for incidents of forced or compulsory labour. | |

| Social assessment of suppliers | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 144 -157 | |

| 103-2 | The management approach and its components | 21; 144 -157 | |

| 103-3 | Valutazione delle modalità di gestione | 21; 144 -157 | |

| 414-1 | Nuovi fornitori che sono stati sottoposti a valutazione attraverso l’utilizzo di criteri sociali | 157 | |

| Public policy | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 107-109 | |

| 103-2 | The management approach and its components | 21; 107-109 | |

| 103-3 | Valutazione delle modalità di gestione | 21; 107-109 | |

| 415-1 | Political contributions | As envisaged by the Code of Ethics, Italgas does not make any direct or indirect contribution in any form to political parties, movements, committees, political organisations or trade unions, nor to their representatives and candidates, except for those specifically mandated by applicable laws and regulations. | 110 |

| Customer health and safety Material issue: Quality and safety of assets | |||

| 103-1 | Explanation of the material topic and its boundary | 21; 99-107; 141-143 | |

| 103-2 | The management approach and its components | 21; 99-107; 141-143 | |

| 103-3 | Evaluation of the management approach | 21; 99-107; 141-143 | |

| 416-1 | Assessment of the health and safety impacts of product and service categories | 100-101 | |

On the basis of the materiality matrix and the table of GRI indicators reported above, below is the table reconciling:

| Minimum elements envisaged by Italian Legislative Decree no. 254/2016 | Document chapters/paragraphs | Capital and material topics | Indicators |

| Corporate management model and organisation of the business activities | | Methodological note | 1. Value creation process in the Italgas Group (paragraphs 1.1 Corporate identity, 1.2 Business model and 1.3 External context, markets and Italgas share) | 3. Governance, risks and opportunities (paragraphs 3.1 Governance, 3.3 The internal control system and 3.4 Ethics and compliance) | 4. Summary data and information (paragraph 4.3 Operating performance) | Responsible governance and risk management Corporate identity Compliance, transparency and fight against corruption Relational capital Human capital | || 405-1 – Diversity of governance bodies and employee |

| Policies practised by the company | | 2. Strategy and forward-looking vision | 5. Italgas Group performance (paragraphs 5.1 Transparent relations, 5.2 Put people at the centre, 5.3 Create value for customers and the market, 5.4 Create value for the territory and the communities and 5.5. Attention to the environment) | ||

| Risk management | | Methodological note (paragraph “Materiality analysis”) | 3. Governance, risks and opportunities (paragraph 3.2 Risk management) | “Information on the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD)” Table | ||

| Use of energy resources Greenhouse gas emissions and polluting emissions into the atmosphere Impact on the environment or other relevant environmental risk factors | | 5. Italgas Group performance (paragraph 5.5. Attention to the environment) | Environmental sustainability Energy transition and the fight against climate change Natural capital | | 302-1 – Energy consumed within the organization | 302-3 Energy intensity | 302-4 – Reduction of energy consumption | 303-3 – Water withdrawals | 303-4 – Water discharge | 303-5 – Water consumption | 305-1 Direct (Scope 1) GHG emissions | 305-2 – Indirect (Scope 2) GHG emissions from energy consumption | 305- 3 – Other indirect (Scope 3) GHG emissions | 305-4 – GHG emissions intensity | 305-5 – Reduction in GHG emissions | 305-7 – Nitrogen oxides (NOx), sulfur oxides (SOx), and other significant emissions | 306-4 – Waste sent for recovery | 306-5 – Waste for disposal | 307-1 – Non-compliance with environmental laws and regulations |

| Impact on health and safety or other relevant health risk factors Personnel management Action taken to prevent discriminatory action or behaviour alute e la sicurezza o altri rilevanti fattori di rischio sanitario Gestione del personale Azioni poste in essere per impedire atteggiamenti e azioni comunque discriminatori | | 5. Italgas Group performance (paragraph 5.2 Put people at the centre) | Protection, inclusion, enhancement and well-being of the human resources Human capital | | 401-1 – New hires and turnover | 403-9 – Accidents at work | 405-1 – Diversity of governance bodies and employees | 405-2 – Ratio of basic salary and remuneration of women to men | 401-3 – Parental leave | 404-1 – Average hours of training per year per employee | 406-1 – Incidents of discrimination and corrective actions taken |

| Social (including those relating to the supply chain and subcontracting and respect for human rights) | | 4. Summary data and information (paragraph 4.2 Key data) | 5. Italgas Group performance (paragraphs 5.1 Transparent relations, 5.3 Create value for customers and the market, 5.4 Create value for the territory and the communities and 5.6 Business outlook (economic-financial) | 6. Comment on the economic and financial results and other information (paragraph 6.2 Comment on the economic and financial results) | Innovation Safety of the networks, assets and people Sustainable supply chain management Quality of service and customer satisfaction Dialogue and the creation of value on the territory Generation of sustainable economic value and ESG finance Intellectual capital Manufacturing capital Relational capital Financial capital | | 308-1 – New suppliers that were assessed using environmental criteria | 414-1 – New suppliers that have been assessed through the use of social criteria | 416-1 – Assessment of the health and safety impacts of product and service categories | 201-1 – Direct economic value generated and distributed | Non-GRI indicator – Value of sponsorships and donations | 207-1 – Approach to taxation | 207-2 – Tax governance, risk control and management | 207-3 – Stakeholder engagement and management | of tax concerns | 207-4 – Country-by-country reporting | 102-7 – Scale of the organisation |

| Respect for human rights | | 2. Strategy and forward-looking vision | 5. Italgas Group performance (paragraphs 5.2 Put people at the centre and 5.3 Create value for customers and the market) | Protection, inclusion, enhancement and well-being of the human resources Sustainable supply chain management Respect for human rights Relational capital Human capital | | 408-1 Operations and suppliers considered to have significant risk for incidents of child labour | 409-1 Operations and suppliers considered to have significant risk for incidents of forced or compulsory labour | 414-1 – New suppliers that have been assessed through the use of social criteria |

| Fight against both active and passive corruption | | 3. Governance, risks and opportunities (paragraph 3.4 Ethics and compliance) | Compliance, transparency and fight against corruption Relational capital | | 205-2 – Disclosure and training on anti-corruption policies and procedures | 205-3 – Confirmed incidents of corruption and actions taken |

9The United Nations Global Compact (GC), the world’s largest voluntary corporate citizenship initiative, requires companies to adhere to principles which encourage

the integration of sustainability in business. Companies/organisations joining the initiative are required to inform all internal and external stakeholders of the

activities undertaken and results achieved during implementation of the Global Compact principles. Participating companies are in fact required to notify

stakeholders on a yearly basis of any progress they have achieved, by publishing an annual reporting document (Communication on Progress, COP) on the GC

website.

10 Please note that for the purposes of non-financial reporting in the Integrated Annual Report, the Italgas Group only includes companies over which Italgas exercises control and not also affiliates that are not subsidiaries, for which the operating data is stated. For the list of companies consolidated using the line-by-line method, please refer to the detail in point “B”) Consolidated financial statements “as at 31 December 2021.